Lev Menand and Joel Michaels (N.Y. Times), Again, Trump Completely Misreads the Law[1]

International trade law is a very, very specialized discipline, and casually thought out opinions are likely to be in error. Viz. my own apparent error.

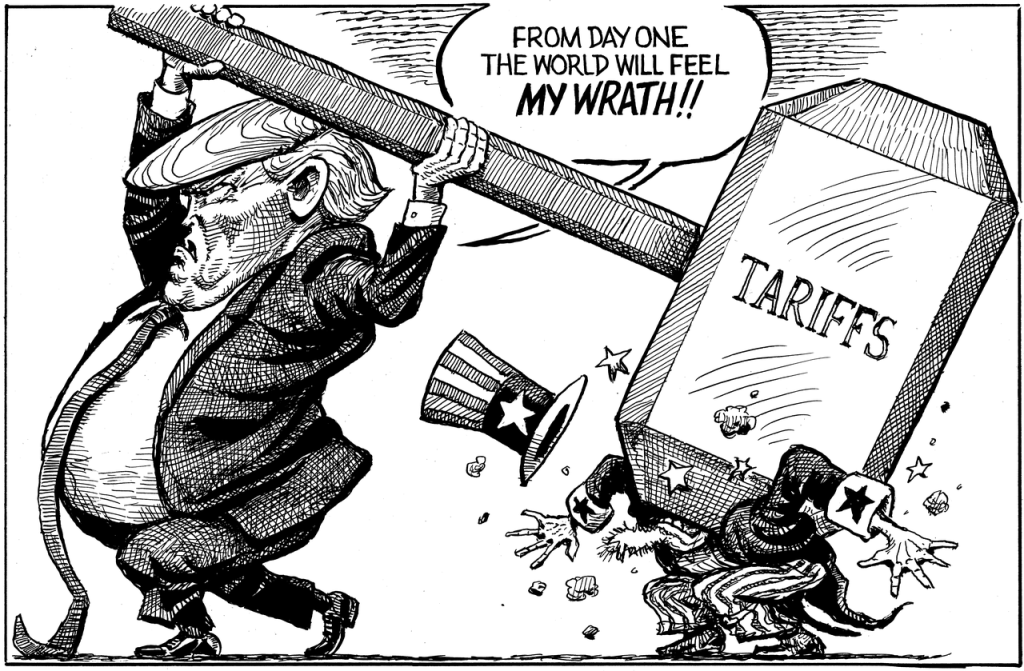

Shortly after the Supreme Court kicked Trump’s ass on Friday of last week, Orange Mussolini took another bite at the apple and purported to invoke Section 122 of the Trade Act of 1974 in order to impose a new set of worldwide tariffs. My impression was that, the second time around, he was on stronger legal ground.

First, unlike the situation with the International Economic Emergency Powers Act of 1977, it’s clear that tariffs are a legitimate tool under Section 122. Second—and here was the big misunderstanding—I thought that the Supreme Court would probably be reluctant to second-guess a presidential finding about an alleged economic emergency, invoked by a President to use authority that Congress had clearly granted to him.

Messrs. Menand and Michaels argue, convincingly, that this is fallacious, because the “emergency” that Trump invoked to employ Section 122 is not the kind of emergency that Section 122 actually addresses. Trump thinks that the Section 122 is all about trade imbalances, whereas, they argue, it’s not about trade imbalances at all, but instead its about financial imbalances. They write,

The provision is not about trade imbalances. Other parts of the statute address those. It is about financial imbalances — in particular ones that threaten financial stability.

The text and context of the law is clear: A Section 122 “payments problem” involves a flight from the U.S. dollar. At the moment, no such problem exists.

The president’s own lawyers essentially admitted as much months ago. In a filing in the earlier case, the Justice Department acknowledged that trade deficits are “conceptually distinct from balance-of-payments deficits,” citing the congressional history. And it suggested that Section 122 did not give the president the authority to impose tariffs to address trade deficits. (Section 122 does not “have any obvious application” where the concerns “arise from trade deficits,” the Justice Department’s lawyers wrote.)

To further appreciate how badly the president is misreading the law, it is necessary to place this particular statute in the context of the early 1970s. …

If you want further elucidation regarding the fascinating topic of financial imbalances, please read the article.

But here’s the bottom line. It’s as if Trump, faced with an emergency caused by foreign killer wasps, has purported to use extraordinary powers granted to the President to address toxic chemical spills.

The issue is not whether the foreign wasps are actually invading, nor is it about deference to the President’s judgment about the magnitude of the wasp problem or the appropriateness of his desired remedy.

The issue is legal, not factual or judgmental, and it has nothing to do with deference to presidential fact finding.

The issue is whether Orange Mussolini is using the wrong damn law as a flimsy cover for another blatant power grab.

[1] Lev Menand in an associate professor at Columbia Law School, so he must be good. Joel Michaels is a Fellow in Public Economic Law at that same institution, my legal alma mater.